Looking for the most important Auditing & Corporate Governance MCQ for your upcoming exams? We have analyzed past papers for CA Final, CS Professional, SEBI Grade A, and CMA Final to bring you the 100 most expected questions. Take the live test, review the blueprint, and master the core concepts.

- 🚀 Updated for 2026: Aligned with the latest CA Final, CS Professional, and SEBI syllabus.

- 🧠 Output & Concept Based: Covers basics to advanced scenarios.

- 📊 Live Gamification: Track your score and time dynamically.

- 📥 Buy PDF: Available instantly via our Telegram channel.

Test Blueprint & Topic Weightage

| Section / Topic | Question Range | Difficulty Level |

|---|---|---|

| SEBI LODR & Corporate Governance Frameworks | Q1 – Q40 | Medium |

| Statutory Audit, NFRA & ICAI Standards | Q41 – Q75 | Hard |

| Specialized Audits, Tech & ESG Disclosures | Q76 – Q100 | Medium to Hard |

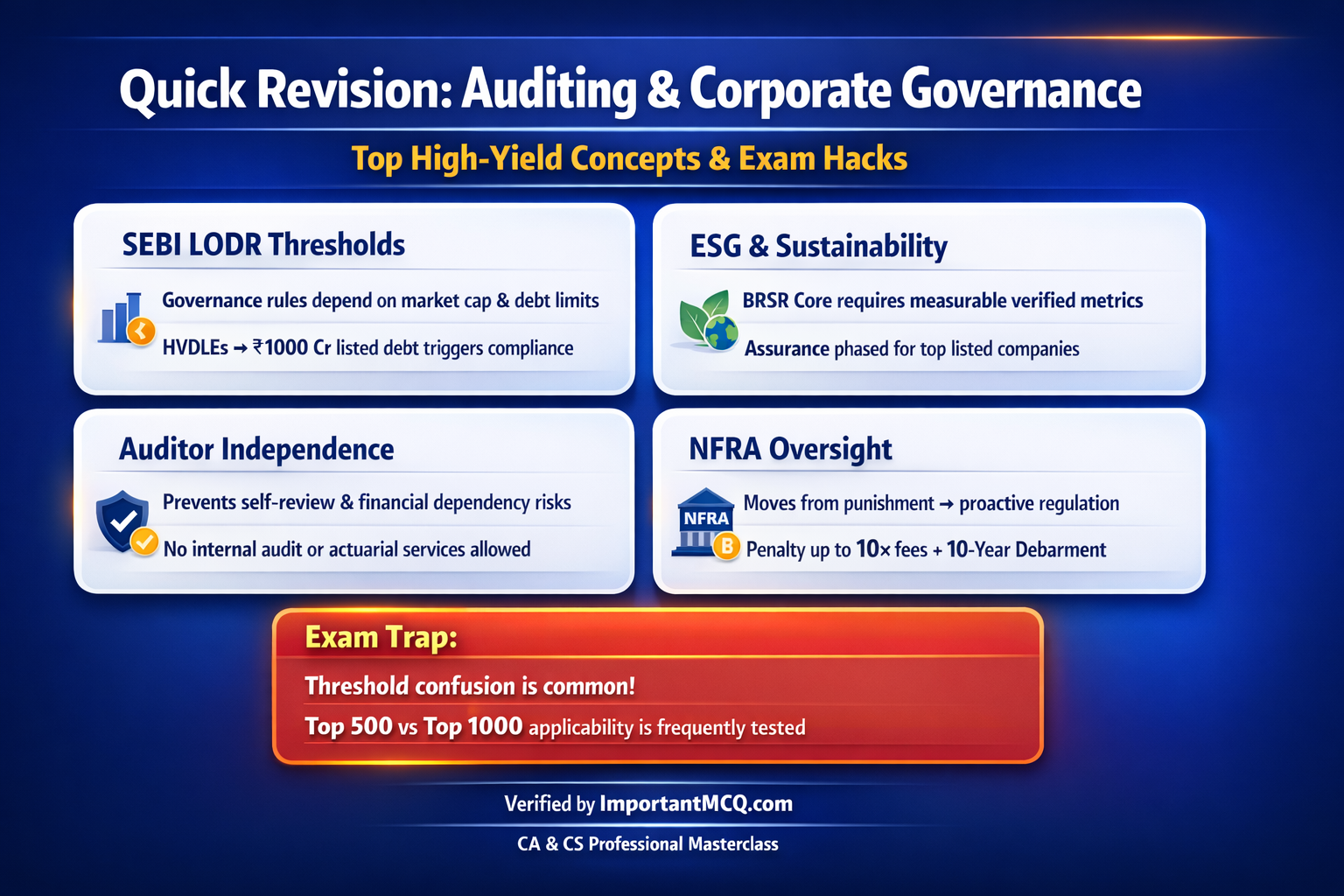

⚠️ Examiner Trap Alert: Examiners frequently trap students by mixing up the financial thresholds and transition timelines for SEBI and Companies Act compliances (e.g., BRSR Core versus general BRSR). Always double-check whether a threshold applies to the “top 500”, “top 1000”, or specific paid-up capital limits, as these are the most common pivot points for incorrect options.

Test Blueprint & Topic Weightage

⏱️ Estimated Time: 150 Minutes | 🎯 Target Score: 80+ | 📊 Difficulty: Moderate to Hard

📚 Interactive Question Bank

Select a question to view the expert explanation and answer.

✅ | SEBI LODR & Corporate Governance Frameworks

Q1Consider the following statements regarding High Value Debt Listed Entities (HVDLEs) under the SEBI (LODR) framework applicable for 2025:Q2Consider the following statements regarding the Business Responsibility and Sustainability Reporting (BRSR) Core framework for the financial year 2025-2026:Q3Consider the following statements regarding the dematerialization of physical securities under the Companies Act for 2025:Q4Consider the following statements regarding the Audit Committee composition for listed entities as per SEBI regulations applicable in 2025:Q5Consider the following statements regarding Related Party Transactions (RPTs) and their materiality thresholds under current SEBI (LODR) Regulations:Q6Consider the following statements regarding the applicability of Secretarial Audit under Section 204 of the Companies Act, 2013 for the year 2025:Q7Consider the following statements regarding ESG disclosures for the Value Chain under the expanded SEBI guidelines for 2025-2026:Q8Consider the following statements regarding Cyber Security Incident Reporting and Board oversight for listed entities as of late 2025:Q9Consider the following statements regarding the rotation of Statutory Auditors under the Companies Act for 2025:Q10Consider the following statements regarding Corporate Social Responsibility (CSR) compliance and impact assessments in 2025:Q11Consider the following statements regarding the Minimum Public Shareholding (MPS) norms mandated by SEBI as of 2025:Q12Consider the following statements regarding the jurisdiction of the National Financial Reporting Authority (NFRA) over unlisted public companies in 2025:Q13Consider the following statements regarding the mandatory appointment of an Internal Auditor for private companies under Section 138 of the Companies Act for 2025:Q14Consider the following statements regarding the Vigil Mechanism (Whistle-blower policy) under corporate governance norms for 2025:Q15Consider the following statements regarding the disqualification of auditors under Section 141 of the Companies Act, applicable in 2025-2026:Q16Consider the following statements regarding the mandatory Joint Audit framework for large Non-Banking Financial Companies (NBFCs) updated for 2025-2026:Q17Consider the following statements regarding Phase IV of the Peer Review Mandate implemented by the Institute of Chartered Accountants of India (ICAI):Q18Consider the following statements regarding the Audit Trail requirements for accounting software under the Ministry of Corporate Affairs (MCA) regulations for 2025:Q19Consider the following statements regarding the regulatory framework for Environmental, Social, and Governance (ESG) Rating Providers (ERPs) formulated by SEBI for 2025:Q20Consider the following statements regarding the reporting of fraud by a statutory auditor under Section 143(12) of the Companies Act:Q21Consider the following statements regarding the applicability of Cost Audit for manufacturing companies in non-regulated sectors for the 2025-2026 cycle:Q22Consider the following statements regarding the applicability of Internal Financial Controls (IFC) for private limited companies in 2025:Q23Consider the following statements regarding the Independent Directors Databank and the online proficiency self-assessment test administered by the IICA:Q24Consider the following statements regarding the Board Evaluation process mandated under the Companies Act and SEBI LODR Regulations:Q25Consider the following statements regarding the tenure and rotation of Secretarial Auditors under the amended Regulation 24A of SEBI (LODR), effective from April 1, 2025:Q26Consider the following statements regarding the transition to Indian Standards on Auditing (IndSAs) proposed by the National Financial Reporting Authority (NFRA) for 2025-2026:Q27Consider the following statements regarding the determination of market capitalization-based compliance requirements under SEBI (LODR) Regulations updated for 2025:Q28Consider the following statements regarding the amendments to Indian Accounting Standards (Ind AS) notified by the Ministry of Corporate Affairs, effective from April 1, 2025:Q29Consider the following statements regarding the Internal Audit Mechanism for Market Infrastructure Institutions (MIIs) mandated by SEBI in May 2025:Q30Consider the following statements regarding the Corporate Laws (Amendment) Bill, 2026 introduced in the Lok Sabha:Q31Consider the following statements regarding the scale-based threshold proposals for material Related Party Transactions (RPTs) under SEBI guidelines for late 2025:Q32Consider the following statements regarding the Strategic Action Plan (2025-2029) issued by the Internal Audit Standards Board of the ICAI:Q33Consider the following statements regarding the adoption of the International Standard on Sustainability Assurance (ISSA) 5000 in India:Q34Consider the following statements regarding the guidelines for the use of Artificial Intelligence (AI) by statutory auditors issued in late 2025:Q35Consider the following statements regarding the initiation of Forensic Audits for classifying Wilful Defaulters under the 2026 RBI Master Directions:Q36Consider the following statements regarding the requirement of Women Directors on corporate boards under SEBI LODR Regulations for 2025:Q37Consider the following statements regarding the Omnibus Approval of Related Party Transactions (RPTs) by the Audit Committee:Q38Consider the following statements regarding the auditor's responsibilities relating to Going Concern under the revised IndSA 570 framework:Q39Consider the following statements regarding the communication of Key Audit Matters (KAM) in the independent auditor's report under SA 701:Q40Consider the following statements regarding the Directors' Responsibility Statement under Section 134(5) of the Companies Act:

✅ | Statutory Audit, NFRA & ICAI Standards

Q41Consider the following statements regarding the comprehensive restructuring of High Value Debt Listed Entities (HVDLEs) under the SEBI (LODR) (Amendment) Regulations, 2026:Q42Consider the following statements regarding the revised definition of a "Small Company" under Section 2(85) of the Companies Act, effective from December 1, 2025:Q43Consider the following statements regarding the Companies (Accounts) Second Amendment Rules, 2025, affecting the Board's Report:Q44Consider the following statements regarding the proposed Ind AS 118 (Presentation and Disclosure in Financial Statements) designed to converge with IFRS 18:Q45Consider the following statements regarding the 2026 SEBI LODR amendments on Investor Services and Physical Securities:Q46Consider the following statements regarding the RBI guidelines for the appointment of Statutory Central Auditors (SCAs) for Commercial Banks for 2025-2026:Q47Consider the following statements regarding the Information Systems Audit Standards (ISAS) introduced by the ICAI in February 2026:Q48Consider the following statements regarding the proposed auditing standards for "Less Complex Entities" (LCEs) finalized by the ICAI in early 2026:Q49Consider the following statements regarding the Structured Digital Database (SDD) requirement under SEBI (Prohibition of Insider Trading) Regulations in 2025:Q50Consider the following statements regarding the Social Audit Standards (SAS) applicable to the Social Stock Exchange (SSE) framework for 2025-2026:

Next 50 →

Page 1 of 2 (100 Total Questions)

High-Yield Core Concepts

High Value Debt Listed Entities (HVDLEs)

A critical aspect of modern SEBI LODR compliance, HVDLEs face strict, mandatory governance provisions if they cross the threshold of Rupees 1000 Crore in listed non-convertible debt.

Business Responsibility and Sustainability Reporting (BRSR)

Core to modern ESG reporting frameworks, this mandate requires the top listed entities to provide reasonable assurance on quantifiable sustainability metrics to prevent greenwashing.

NFRA Jurisdiction & Penalties

The National Financial Reporting Authority actively oversees large unlisted public companies based on strict Statutory Audit limits and holds draconian penalty powers (up to 10x audit fees) for professional misconduct.

NOCLAR (Non-Compliance with Laws and Regulations)

A cornerstone of ICAI professional ethics, this requires auditors to report a client’s severe legal violations to external authorities, overriding traditional client confidentiality in the public interest.

Semantic Comparison

| Feature / Metric | Auditing & Corporate Governance | Financial Accounting |

|---|---|---|

| Core Definition | Independent verification & ethical oversight of corporate operations. | Recording, summarizing, and reporting daily financial transactions. |

| Primary Use Case | Ensuring compliance, transparency, and shareholder protection. | Preparing balance sheets, P&L statements, and cash flows. |

| Exam Importance | Heavy on theoretical provisions, limits, timelines, and penalties. | Heavy on numerical calculations, formats, and journal entries. |

Frequently Asked Questions

Why is Auditing & Corporate Governance MCQ critical for CA Final and CS Professional?

It is a consistently high-scoring area. Examiners frequently repeat core concepts from this section, particularly focusing on recent amendments to SEBI LODR and the Companies Act.

Does this mock test cover the full syllabus?

Yes, these questions target the most highly-weighted concepts found in previous years’ papers, including recent changes to the ICAI Code of Ethics and NFRA guidelines.

What are the most repeated topics?

Based on our blueprint, SEBI LODR & Corporate Governance Frameworks and Statutory Audit regulations carry the highest weightage.

Best Practice Auditing & Corporate Governance MCQ. Thank You.